© 2016–2026 Sixty Two team · PT Plus Enam Dua

A modern approach to Islamic Digital Banking.

UI UX Exploration

Unfolding today's Islamic Digital Banking

customer needs

Islamic banking concept is not new in Indonesia. Since the 90s, Bank Muamalat has opened the first existence of a bank operating based on the Islamic Sharia in Indonesia. Then, other Islamic banks started to flourish (Bank IFI, Mandiri, Niaga, BTN, Bank Mega, Bank BRI, Bank Bukopin, BPD Jabar, BPD Aceh, etc.), pushing the government to finally establish its official sharia banking regulations in Indonesia.

Today, around 30 million Indonesian use Islamic banking (according to Bank Syariah Indonesia in November 2020). Yes, it is still a relatively small number compared to the total Muslim population in Indonesia, which is 180 million people. In order to understand better why this group chose Islamic banking and how the experience looks like, we conducted interviews with some Islamic banking users in our circle.

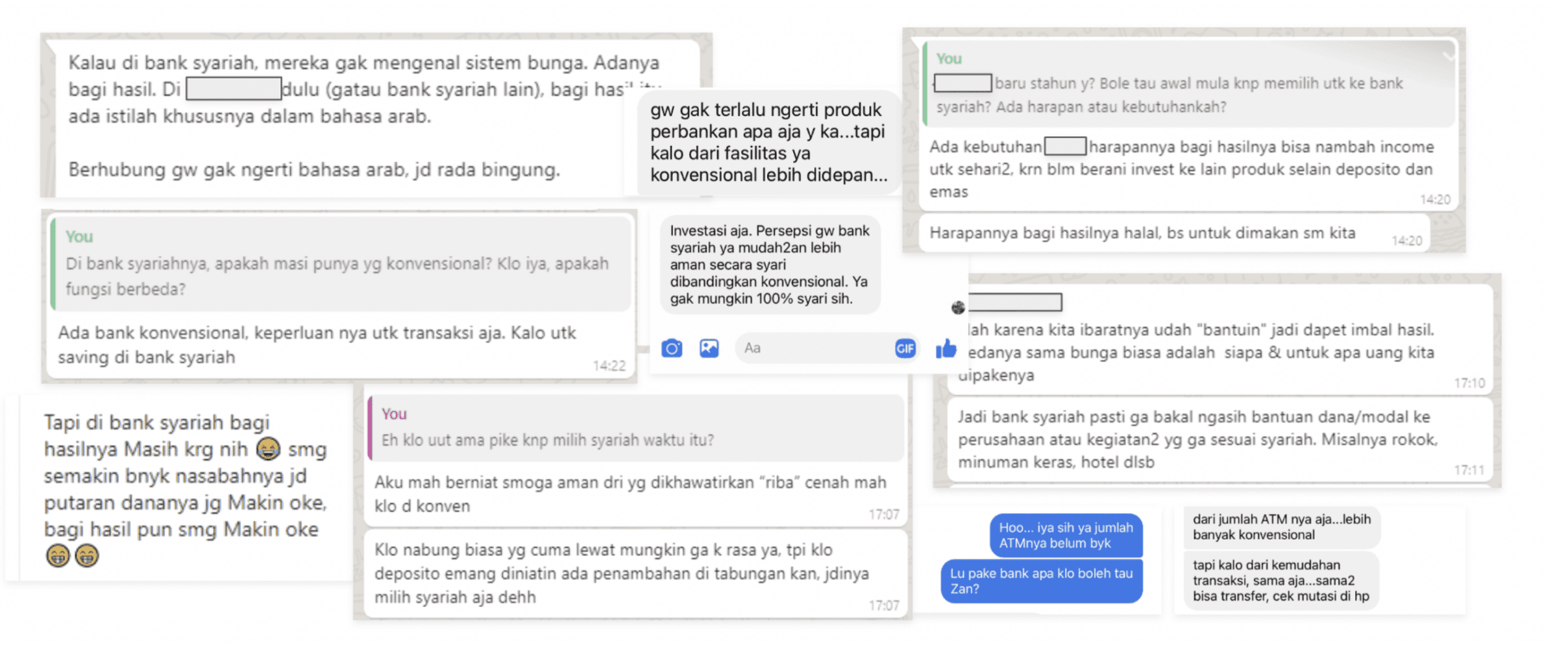

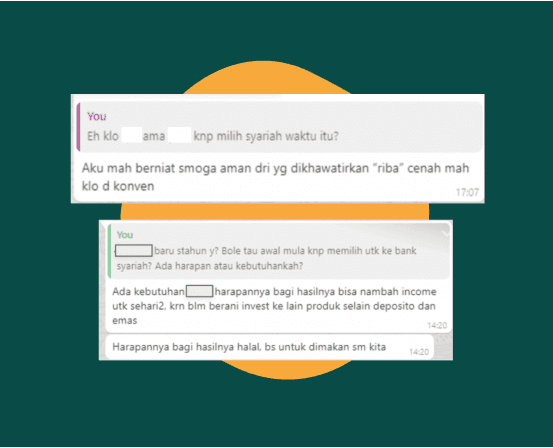

- Sharia banking means users don't have to compromise their faith & ethical values.

As opposed to the conventional banking way of having bank interest, Islamic Banking is about fair profit sharing. Not only that, all the ethical rules, procedures and guidelines that are based on the Islamic sharia—one of them is not to include all uncertain objects (gharar), contain gambling (maysir) and unjust (zalim). These values are the things that, for some Muslim groups, are not to be discounted. For them, doing banking in a conventional way means they have to compromise their faith and ethical values. In a nutshell, Islamic Banking is a halal way of conducting a financial activity so that it would produce a halal living; as quoted by one of our interviewees:

- Ethical & transparent financial activity information

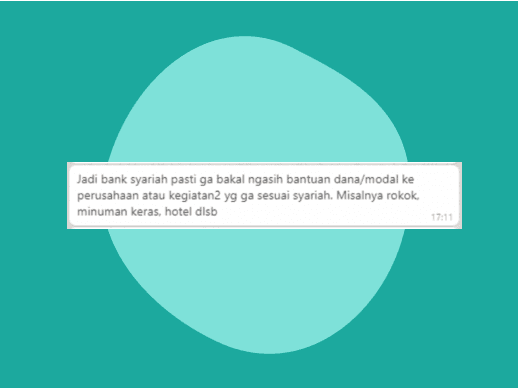

Islamic banks do not invest in goods and services that are contrary to Islamic sharia, such as investments in alcohol brands, pork products, pornography, gambling, military equipment, or weapons. Furthermore, it gives corporate and regulatory transparency; disclose the risk, challenge, and breakthrough the bank has made.

By stating contracts in Islamic banking clearly and transparently, it gives a sense of security as it is intended to help customers feel comfortable keeping their funds safe, without the risk of uncertainty (gharar) and interest (riba).

- Islamic banking customers still feel the need to open a conventional bank account since it is perceived as superior.

Interestingly, all of the Islamic banking customers whom we interviewed also use conventional banks along with Islamic banks. This happens because of the high popularity of conventional banking for transactional purposes. In particular, the conventional banking sector plays a crucial role in promoting savings, investments, and trade by serving as a financial intermediary.

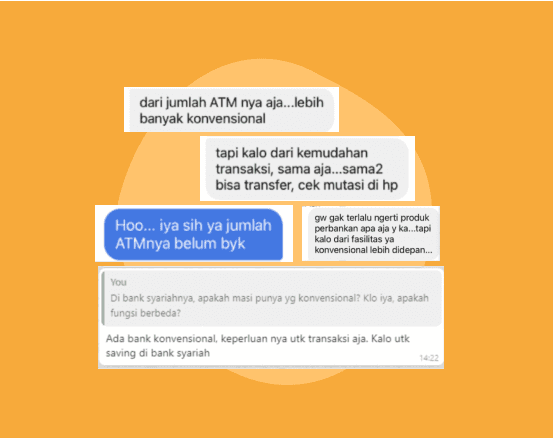

- Conventional bank facilities are perceived to be more accessible

Customers perceived that they couldn't use conventional ATMs for sharia account services from the same bank. Conventional bank accounts are still popular and preferable for transactional purposes because merchants (online/offline) widely accept conventional banks compared to Islamic banks.

- Lack of understanding on the full offerings due to barriers in understanding various terminologies

The use of sharia terms & jargon sometimes confuses users, making them unable to fully comprehend the Islamic bank's services. There are also some different uses of terms in different Islamic banks. This has led to the gap in users' awareness of the full extent of the offerings.

How might we better serve these unique needs in the digital space?

With those insights in mind, we explored the added values that could be achieved by today's digital solution. As mentioned in Generation M book by Shelina Janmmohamed, they are tech-savvy, conservative in their religious practice while incorporating a modern approach to their lifestyle. Thus, we redefined how a digital companion like a personal digital bank that aligns with personal faith could add value beyond its financial functions. After all, the first motivation for using Islamic banking is its halal living goal.

Digital consumers have high and ever-increasing expectations of the customer experience they expect from companies and how they want to be engaged. These consumers expect timely and relevant engagement. We pinpointed several key behavior areas that responded to halal living goals and put them at the center of the proposed design solution—offering relevant engagement to the modern-day Muslim.

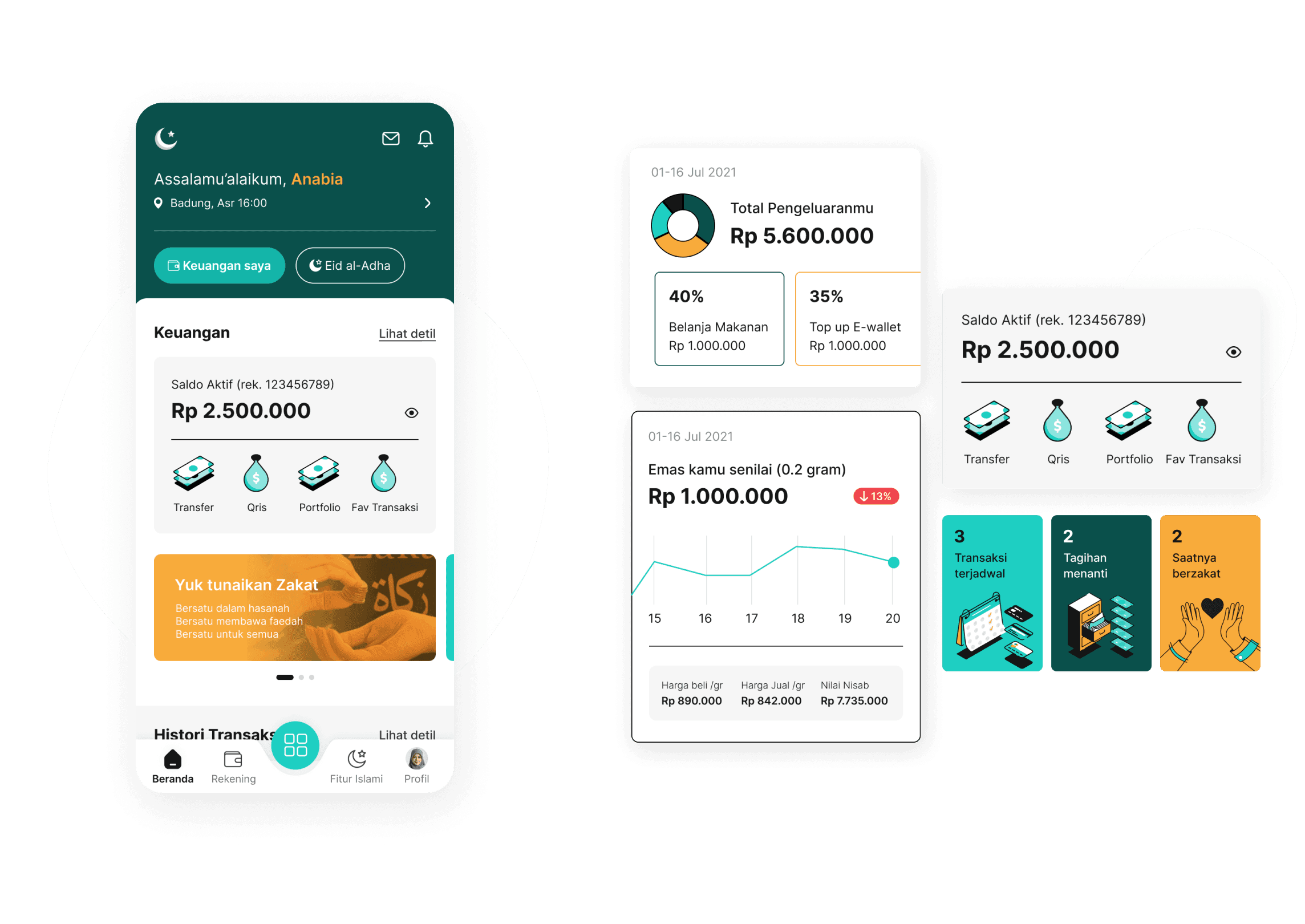

- An insightful platform that knows you.

People's financial behavior may differ from person to person. Even though this user group may share the same faith and ethical values, a preference for what interests them more in terms of financial insights could be different. We observed that some people are more inclined to have more insights on halal investment, while others are more into a reminder of Islamic events or prayer.

Here, purposeful content and personalization approaches play roles in responding to users' different habits, usage and preferences. It allows financial institutions to develop long-term and genuine relationships with users.

Through the modular approach, the interface would change and adapt to the users' habits, not just simply by showing them relevant tiles. The content would also adjust with the user as they use it. This way, their personal preferences are easily displayed based on their habits, allowing them to personalize & prioritize the right content for them.

- Elevating Islamic banking experience: from financial to social and spiritual companion

Putting Muslim customers narratives as the main ingredients, we looked into other Muslim activity areas that could support their intention towards halal living. From finance-related activity to social and spiritual practice, our intention is to design an experience that puts them first.

Purposeful & transparent financial activity

Trust is the most essential currency in Islamic Finance services. Thus, providing greater transparency on financial aspects makes customers feel more secure about storing their funds.While our audience is already familiar with the common financial features to do savings effectively, we extend this familiar concept to help them do their financial activities, according to what Islamic teaching suggests (zakat, qurban, etc.)

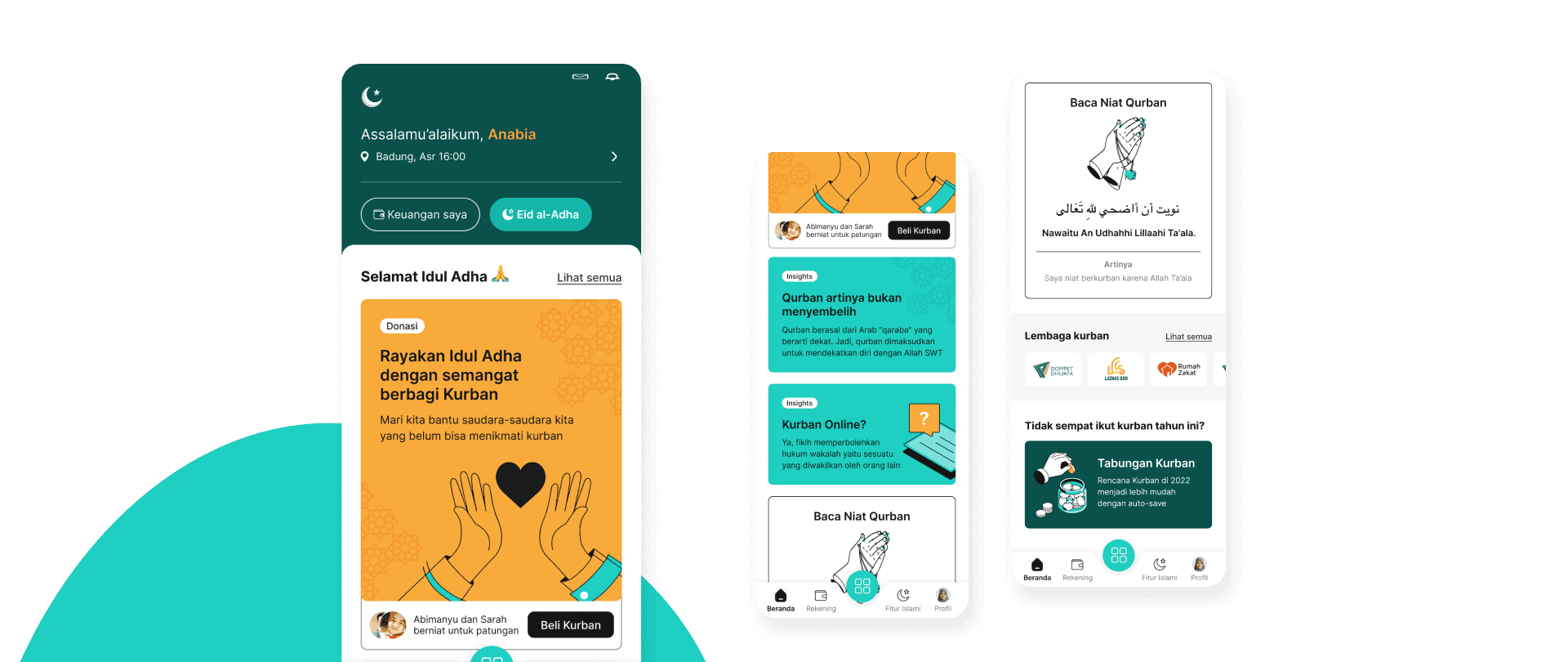

Integrating financial, social & spiritual aspects in a meaningful way

We took one of the biggest financial spendings for a Muslim to explore this. Let's take Eid al-Adha, for example, when affluent Muslims make Qurbani donations to communities in need by sacrificing animals like cows and goats. A perfect moment where one of the biggest Islam celebrations that blend festivity and financial activity.Exploring this, we visioned a dedicated section on the home page that focuses on Islamic activities and celebrations. Providing relevant information and insights on the current events and inviting people to share their experiences with each other. The contextual knowledge will help give an understanding of literacy on jargon or specific terms that will enrich their knowledge on the subject.

Responding to the current Indonesian behaviour on collectively purchasing animals (cows or goats) for Qurban, we extend the idea into a social activity in a digital platform where users can find people within their circle that are interested in joining their qurban purchase.

Furthermore, contextually relevant prayers on the sections will provide a meaningful experience in response to the religious practice.

Conclusions

The future of Islamic finance is wide open and ripe for disruption, driven by a tech-literate generation. To provide a service that aligns Islamic values with the modern lifestyle is an exciting yet challenging opportunity. Starting by acknowledging fundamental values that are important for Generation M, it is essential to translate them into a simple, friendly experience to fill the information barrier gap. Turning them into a financial, social, and spiritual companion, all in one solution.

Through this case study exploration, we aim to open up a new conversation that respects all faith and values as part of our inclusivity agenda. Looking deeper into this topic has pushed our team's boundaries and allowed us to explore new exciting territory! Moreover, if we could apply the exploration into real design and solutions. We believe that a great exploration comes from great collaboration as well. If you're looking for a curious partner to explore great topics together, we are just an email away. Learn more about Sixty Two's case study explorations and our report on inclusive design in Southeast Asia.

Let’s collaborate!

Whether you have a project you would like to chat about, looking to work with us, or want to get to know us.